Understanding how much retirees earn across different ages and states is more important than ever as living costs continue to rise nationwide. New 2026 estimates show wide differences in retirement income depending on age, location, and access to Social Security, pensions, and private savings. These insights help millions of Americans measure their own retirement readiness and understand where retirees enjoy the strongest financial stability.

How Retirement Income Changes as Americans Age

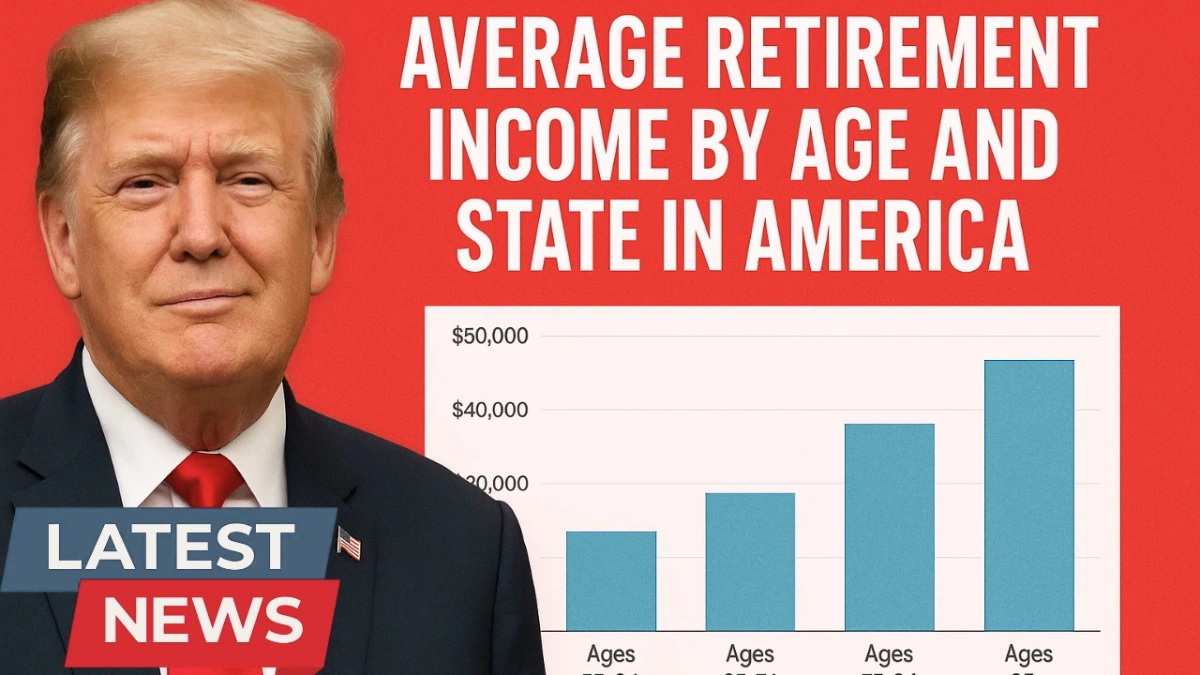

The data shows income tends to peak shortly after retirement, with many households in the 65–74 range reporting the highest earnings due to Social Security benefits, part-time work, and access to pensions or retirement savings. Income naturally declines after age 75 as older adults reduce work activity and begin using retirement funds more conservatively. Medical costs also rise in later years, impacting disposable income despite Social Security adjustments.

| Age Group | Average Annual Retirement Income (National) |

|---|---|

| Ages 60–64 | ~$53,000 |

| Ages 65–74 | ~$55,000 |

| Ages 75+ | ~$43,000 |

The Role of Social Security in Total Retirement Income

For the majority of retirees, Social Security makes up 40% to 90% of total income, depending on savings and state of residence. In lower-income states, Social Security often represents the primary source of support. In wealthier states, retirees typically combine Social Security with pensions, investments, and part-time earnings, creating a higher overall income level. The average monthly Social Security benefit sits near $2,000, but retirees with higher lifetime earnings can receive far more.

States With the Highest Retirement Income

States such as Maryland, Connecticut, New Jersey, Massachusetts, Virginia, and California consistently rank among the highest for retirement income. These areas benefit from stronger pension availability, higher historical wages, and more retirement savings among residents. Retirees in these states often report incomes well above the national average, with some regions exceeding $70,000 per year.

States With the Lowest Retirement Income

Retirees in Mississippi, Arkansas, West Virginia, New Mexico, and Kentucky report some of the lowest average incomes. These states rely heavily on Social Security, with fewer residents having large savings or pension benefits. Lower wages during working years also contribute to reduced Social Security payouts in retirement. However, these states often offer lower housing and living costs, allowing retirees to stretch their income further.

How Cost of Living Shapes Retirement Quality

A retiree earning $50,000 per year in one state may feel financially secure, while another earning the same amount in a high-cost state like California or New York may struggle. States with lower housing costs, lower taxes, and affordable healthcare enable retirees to maintain a better lifestyle even with smaller incomes. This is why many older Americans move to more affordable locations during their retirement years.

The Growing Importance of Supplemental Income

More retirees than ever are working part-time to supplement Social Security. This trend is strongest among adults aged 62–69, many of whom choose phased retirement to cushion their savings and delay tapping into long-term investments. Part-time work also helps retirees delay claiming Social Security, which increases their lifetime benefit amount.

Retirement Income Gaps Between Men and Women

Women typically earn less over their lifetimes due to wage gaps and career breaks for caregiving, which results in lower Social Security benefits. As a result, retired women often report incomes 15–20 percent below those of men. This highlights the importance of early planning, spousal benefits, and catch-up contributions for women nearing retirement.

Planning for a Stronger Retirement in Any State

Regardless of where someone lives, maximizing retirement income requires strong planning. Saving early, delaying Social Security when possible, maintaining part-time earnings, and reducing debt before retirement all help build long-term financial stability. Location decisions also matter — retirees who move to states with lower taxes and more affordable housing often see their quality of life improve even without large incomes.

Conclusion:

The average retirement income in America varies widely by age and state, but the national trend shows that most retirees rely heavily on Social Security supplemented by savings, pensions, or part-time work. Higher-cost states require significantly more income to maintain comfort, while lower-cost regions allow retirees to stretch their dollars further. Understanding these differences helps individuals plan more effectively and make decisions that support long-term financial security.

Disclaimer: Retirement income estimates are based on national surveys and financial projections. Individual income levels vary depending on work history, Social Security records, pension eligibility, savings amounts, and state-specific cost-of-living factors.